AML and KYC in crypto are no longer topics only for compliance officers. If you work for a crypto exchange, wallet provider, fintech platform, stablecoin company, crypto payment firm, blockchain analytics provider, or digital asset startup, you need to understand the basics.

AML stands for Anti-Money Laundering. KYC stands for Know Your Customer. Together, they help digital asset firms reduce financial crime risk, verify customers, detect suspicious behavior, and protect the business from misuse.

Crypto creates unique risks because transactions can move across borders in minutes. Wallet addresses may not show a person’s real name. Criminals may also use crypto to move stolen funds, hide illicit proceeds, bypass sanctions, or scam victims. Therefore, every digital asset employee should know what red flags look like, when to escalate concerns, and how their role supports a safer crypto business.

What Do AML and KYC Mean in Crypto?

AML means Anti-Money Laundering. In crypto, AML controls help stop criminals from using digital assets to move, hide, convert, or disguise illegal funds.

For example, a criminal may move stolen crypto through several wallets, swap it into another token, send it to an exchange, and cash out into fiat currency. AML controls help firms detect this activity before the platform is misused.

KYC means Know Your Customer. It is the process of identifying and verifying customers. A crypto exchange may ask for a government ID, selfie check, address details, or business documents before allowing certain services.

KYC is part of the wider AML process. It helps the firm understand who the customer is. However, AML goes further. It may include customer risk ratings, sanctions screening, wallet screening, transaction monitoring, investigations, reporting, and recordkeeping.

For instance, a customer may pass KYC during onboarding. Later, their transaction behavior may become unusual. As a result, the firm may need to review the account, ask more questions, or escalate the case.

Why AML and KYC Matter in Digital Asset Firms

AML and KYC matter because crypto platforms can be attractive to criminals. Digital assets move quickly, and some users may believe crypto is harder to trace than traditional money. However, many blockchain transactions are public, and firms can use monitoring tools to identify risky patterns.

AML and KYC help prevent money laundering, terrorist financing, sanctions evasion, ransomware payments, fraud, scam activity, and darknet market exposure. They also help protect customers from harm.

For example, a customer may be tricked into sending crypto to a fake investment platform. If a support employee recognizes scam indicators, the firm may be able to slow the process, escalate the concern, or guide the customer to safer support channels.

Strong AML and KYC controls also support trust. Banks, payment partners, regulators, investors, and enterprise clients often expect digital asset firms to show that they understand financial crime risk.

Global and US Compliance Context

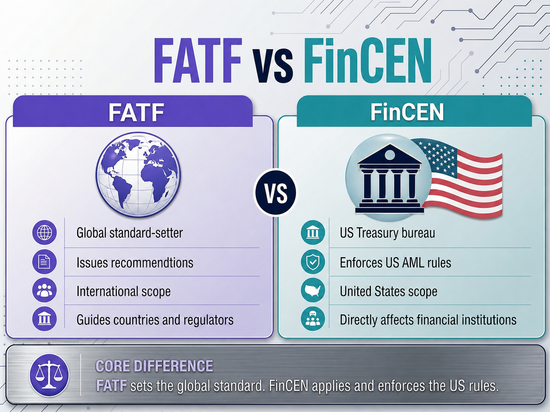

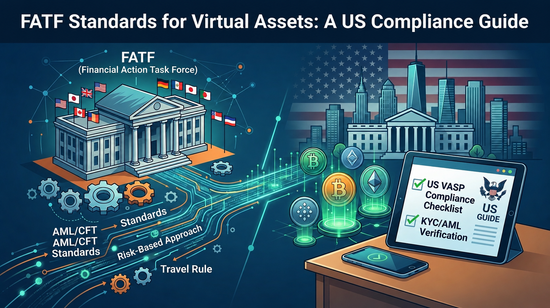

Crypto compliance is shaped by global standards and local laws. Globally, the Financial Action Task Force, known as FATF, sets standards for Anti-Money Laundering and Counter-Terrorist Financing. FATF expects countries to apply AML/CFT rules to virtual assets and virtual asset service providers.

In the United States, FinCEN has explained that certain businesses dealing with convertible virtual currency may be money services businesses under the Bank Secrecy Act. OFAC is also important because sanctioned people, groups, jurisdictions, or wallet addresses may try to use digital assets.

Employees do not need to memorize every rule. However, they should understand why checks exist, follow company policies, and escalate unusual activity when needed.

How AML and KYC Work in Practice

AML in crypto usually starts with a risk-based approach. This means a firm should apply stronger controls where the risk is higher. Risk can depend on customer type, country, product, wallet exposure, transaction size, payment method, business model, and expected activity.

AML includes onboarding controls. Before customers can trade, deposit, withdraw, or access certain features, the firm may collect information and verify identity. However, AML does not stop after onboarding. Firms also monitor customer behavior over time. A low-risk customer may suddenly start sending large amounts to risky wallets, which may trigger another review.

Suspicious activity escalation is another key part of AML. Employees should know when to raise a concern and what details to include, such as customer ID, transaction information, messages, wallet addresses, and reasons for concern.

KYC helps a firm understand who is using its services. For individuals, KYC may include name, date of birth, address, government ID, selfie checks, device data, and sanctions screening. For business customers, it may include company documents, directors’ details, beneficial owners, business activity, source of funds, and expected transaction volume.

In crypto, KYC may also connect with wallet and transaction risk. A customer may be verified as a real person, but their wallet activity may still show exposure to scams, hacks, mixers, or sanctioned entities. Therefore, identity checks alone are not enough.

CDD, EDD, Wallet Screening, and Monitoring

CDD stands for Customer Due Diligence. It means understanding who the customer is, what they do, why they use the service, and whether their activity makes sense.

EDD stands for Enhanced Due Diligence. EDD means deeper checks for higher-risk customers or activity. This may include source of funds checks, senior approval, extra documentation, or closer monitoring.

Customer risk can change over time. Therefore, risk ratings should not be treated as fixed forever. For employees, the key lesson is simple: customer risk is about documents, behavior, context, and changes over time.

Wallet screening is another major part of crypto compliance. A wallet address may not show a person’s real name, but it can still show links to sanctioned wallets, scams, ransomware, darknet markets, mixers, stolen funds, hacks, exploits, or high-risk services.

Transaction monitoring looks at patterns of activity. A firm may flag sudden spikes in volume, rapid deposits and withdrawals, transfers to high-risk wallets, or activity that does not match the customer profile.

However, tools are not enough by themselves. A system may raise an alert, but trained staff need to review the context. Sometimes an alert has a reasonable explanation. In other cases, the firm may need to restrict activity, ask questions, or escalate the case.

Sanctions and Red Flags Employees Should Know

Sanctions risk is especially important in crypto because digital assets can move across borders quickly. Sanctions may apply to individuals, companies, groups, countries, services, or wallet addresses. Therefore, crypto firms often screen customers and wallets against sanctions-related data.

Employees should know that sanctions risk is serious. If a wallet is linked to sanctioned activity, staff should not ignore the alert or try to solve it informally. Instead, they should follow the firm’s escalation process.

Common AML and KYC red flags include fake or altered ID documents, inconsistent names or addresses, multiple accounts using similar details, refusal to provide information, suspicious device patterns, and customers asking how to avoid checks.

Other red flags include unusual urgency, large activity soon after account opening, rapid deposits and withdrawals, transfers to high-risk wallets, activity that does not match the customer profile, and repeated small transactions below review thresholds.

Scam victim red flags are also important. A customer may say they are sending funds to an online investment manager, a new romantic partner, a recovery service, or someone giving instructions over the phone.

How Different Teams Support AML and KYC

Customer support teams can spot scam victims, suspicious questions, pressure tactics, and unusual customer behavior. Onboarding and operations teams review documents, verify information, apply risk ratings, and escalate inconsistencies.

Compliance and AML teams manage alerts, investigations, reporting, risk assessments, policy controls, and regulatory communication. However, they rely on other teams to send good information.

Product and engineering teams design onboarding flows, monitoring triggers, data capture, risk controls, and escalation workflows. Marketing teams support compliance by avoiding misleading claims. Finance teams may notice unusual fiat flows, chargebacks, payment mismatches, or reconciliation issues. Leadership teams set the tone across the business.

Common AML and KYC Mistakes in Crypto Firms

One common mistake is treating KYC as a one-time task. Customer risk can change after onboarding, so firms need ongoing monitoring.

Another mistake is collecting documents without understanding risk. KYC is not just a file collection exercise. Employees need to understand what the information means.

Ignoring wallet risk is also dangerous. A customer may pass identity checks but still interact with high-risk wallets. Some firms also over-rely on automation, even though tools can miss context and human review still matters.

Weak escalation routes create another problem. If employees do not know who to contact, concerns may be delayed or ignored. Finally, many firms fail to train non-compliance staff, even though risk can appear across the business.

Practical Scenarios for Digital Asset Employees

A customer at a crypto exchange asks support whether there is a way to trade without completing verification. A trained support agent knows this should be escalated.

A wallet provider receives crypto from a wallet linked to a known scam cluster. The screening tool flags the deposit, and operations staff send the case to compliance.

A possible scam victim asks how to send crypto quickly to someone they met online who promised investment returns. A trained employee recognizes possible scam indicators and follows the escalation process.

How to Build AML and KYC Awareness Across Your Team

Start with baseline training for all employees. Everyone should understand AML, KYC, CDD, EDD, sanctions, wallet screening, transaction monitoring, red flags, and escalation.

Next, add role-specific examples. Support teams need scam scenarios. Operations teams need onboarding cases. Product teams need control design examples. Marketing teams need communication examples.

Use scenario-based learning whenever possible. Employees learn faster when training reflects real customer and transaction situations.

Create clear escalation workflows. Staff should know who to contact, what details to include, and how quickly to act. Also, refresh training regularly because crypto risks, scams, sanctions, and typologies change over time.

Final Thoughts: AML and KYC Are Everyone’s Responsibility in Crypto

AML and KYC are not just compliance department tasks. They support customer safety, business trust, regulatory readiness, and responsible growth.

As digital asset firms grow, employees across every department need practical awareness. Support teams may spot scam victims. Operations teams may catch onboarding issues. Product teams may design safer controls. Marketing teams may prevent misleading claims. Leadership teams may set a stronger culture.

Therefore, every digital asset firm should train employees on the basics of AML and KYC. Staff do not need to become legal experts, but they should know how to recognize risk, follow procedures, and escalate concerns.

Start Learning AML and KYC in Crypto

The Crypto Compliance Fundamentals For All Staff In Digital Asset Firms course introduces AML, KYC, CDD, EDD, sanctions, transaction monitoring, wallet risk, customer risk, red flags, and escalation responsibilities in clear, beginner-friendly language.

Whether you are training one employee or building awareness across a full digital asset team, this course gives staff the language, context, and confidence to understand AML and KYC in everyday work.

Explore the course today and help your team build stronger crypto compliance awareness from the ground up.