Crypto exchanges verify customers by collecting identity details, checking documents, screening users, assessing risk, and monitoring activity after onboarding. However, customer verification is more than uploading an ID. It connects KYC, customer due diligence, fraud controls, sanctions screening, and blockchain risk checks so exchanges can understand who is using the platform and whether their activity makes sense.

In practice, onboarding starts with registration and continues through identity checks, wallet screening, manual review, approval decisions, and ongoing monitoring.

How Do Crypto Exchanges Verify Customers?

Crypto exchanges verify customers through a step-by-step onboarding process. First, the customer creates an account. Next, the exchange collects identity information, checks documents, screens the user, assesses risk, and decides whether to approve, restrict, or reject the account.

Some checks are automated, but tools cannot handle every case. If a document, selfie, or risk signal looks unusual, an analyst may need to review the case manually.

Crypto verification is stricter than a normal app signup because an exchange account can move real value quickly. Therefore, exchanges need stronger controls to reduce fake accounts, detect high-risk users, and prevent financial crime.

Why Customer Verification Matters in Crypto

Customer verification matters because crypto can be misused for money laundering, fraud, sanctions evasion, scams, and account abuse. For example, a fraud network may use stolen IDs to create many accounts, move scam proceeds, and withdraw funds before the exchange reacts.

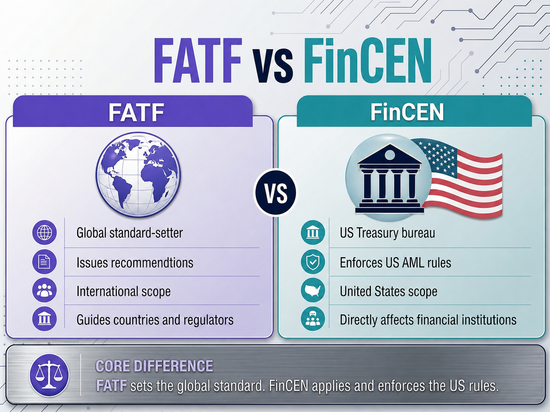

In the US, some digital asset businesses may fall under Bank Secrecy Act obligations. Globally, FATF expects virtual asset service providers to apply customer due diligence, recordkeeping, suspicious reporting, and transfer-related information controls.

Sanctions risk is also important because OFAC rules apply to crypto and traditional finance. Chainalysis reported that known illicit crypto addresses received at least $40.9 billion in 2024, so exchanges need systems that detect risky activity early.

Step 1: Account Registration and Initial Checks

Verification usually starts when a customer creates an account. They may enter an email address, phone number, password, country of residence, and date of birth. The exchange may also ask the customer to accept terms and confirm they meet the minimum age requirement.

At this stage, it may check restricted countries, suspicious emails, reused phone numbers, repeated devices, and high-risk login locations.

Step 2: Identity Verification and Document Review

After registration, the exchange usually asks the customer to complete identity verification. This is the core KYC stage. For individuals, common information includes full legal name, date of birth, residential address, phone number, email address, and country of residence. Some exchanges may also request tax details, occupation, or expected account activity.

Next, the customer may upload a government-issued ID, such as a passport, driver’s license, state ID, or national identity card. The system may check the document type, expiry date, photo, name, date of birth, and security features. Many exchanges also use selfie or liveness checks.

Proof of address may also be required. Verification can fail if the document is blurry, expired, altered, unsupported, or mismatched. The exchange may request better documents or send the case for manual review.

Step 3: Customer Due Diligence and Risk Assessment

Customer Due Diligence, or CDD, goes beyond checking identity. It helps the exchange understand the customer’s risk. CDD asks practical questions: Why does the customer want to use the exchange? What activity is expected? Where do the funds come from?

For example, a retail user may plan to buy small amounts of Bitcoin each month. However, if the same user suddenly receives large stablecoin deposits from several wallets, the exchange may reassess the customer.

Risk factors may include location, occupation, business type, expected volume, source of funds, payment method, wallet exposure, and prior fraud signals. As a result, customers may be rated low, medium, or high risk.

Step 4: Sanctions, PEP, and Adverse Media Screening

Crypto exchanges also screen customers against risk lists. This usually includes sanctions screening, politically exposed person screening, and adverse media checks.

Sanctions screening helps identify whether a customer may match a sanctioned person, entity, country, or blocked party. For US-facing businesses, OFAC sanctions risk is especially important.

PEP screening looks for politically exposed persons. Being a PEP does not always mean rejection, but it can increase bribery, corruption, or reputational risk. Adverse media screening checks negative news linked to fraud, cybercrime, corruption, sanctions evasion, scams, or other serious risks. Because common names can create false positives, analysts must compare identifiers before making a decision.

Step 5: Wallet Screening and Blockchain Risk Checks

Crypto exchanges also need to understand wallet risk. This is where crypto verification becomes different from traditional finance. A customer may pass identity checks but still interact with risky wallets, such as wallets linked to scams, darknet markets, ransomware, mixers, stolen funds, or sanctioned addresses.

Wallet screening tools help exchanges review where funds came from, where they are going, and whether the wallet has exposure to known illicit activity. For example, a verified customer deposits stablecoins from a wallet with recent exposure to a phishing scam. The identity may be valid, but the deposit source creates risk.

Therefore, crypto exchanges should combine KYC data with blockchain risk data instead of relying only on identity documents.

CTA Block: Build Practical KYC and CDD Skills

Want to understand how customer verification works inside real crypto exchange environments? Explore the How Crypto Exchanges Verify Customers: KYC, CDD and Onboarding Explained course. This course covers identity verification, CDD, onboarding decisions, sanctions screening, wallet risk, failed verification cases, and practical workflows.

Step 6: Manual Review, Approval, or Rejection

Automated tools can speed up onboarding, but they cannot handle every case. Manual review is needed when the system finds something unusual, such as document mismatch, unclear ID images, possible sanctions matches, suspicious device behavior, high-risk wallet exposure, or inconsistent customer answers.

During manual review, analysts may check the ID, profile, screening results, wallet exposure, source of funds evidence, explanations, previous activity, and linked accounts. The customer may then be approved, limited, asked for more information, restricted, escalated, rejected, or closed.

Communication also matters. Exchanges should use clear and neutral language, such as “We need additional information to complete your review.”

Step 7: Ongoing Monitoring After Onboarding

Customer verification does not end when the account is approved. Customer risk can change over time. A customer may start with small purchases and later move large amounts. A business may change ownership. A wallet may later be linked to a scam or sanctioned address.

Periodic KYC refresh may include updating ID documents, confirming address details, reviewing source of funds, refreshing business ownership, or re-screening customer risk. Event-triggered reviews may happen after unusual logins, large crypto deposits, risky withdrawal wallets, or investigation links.

KYC and transaction monitoring work together. KYC tells the exchange who the customer is. Transaction monitoring shows what the customer is doing. Together, they help analysts decide whether activity is normal or suspicious.

Individual vs Business Account Verification

Individual verification is usually simpler than business verification. For individuals, the exchange checks identity, address, date of birth, ID documents, selfies, and source of funds where needed.

Business verification is more complex. The exchange may need company registration documents, business address, ownership structure, beneficial owner details, directors, authorized users, business model, expected transaction volume, and source of funds.

Common Customer Verification Red Flags

Customer verification red flags can appear at any stage. Identity red flags include expired IDs, altered documents, mismatched names, repeated selfie failures, or inconsistent dates of birth. Account red flags include many accounts from one device, disposable email domains, shared phone numbers, VPN use with mismatched location, or rapid withdrawal attempts after signup.

Behavioral red flags include customers who refuse to explain source of funds, pressure support teams to bypass checks, give inconsistent answers, or claim they are acting for someone else. On-chain red flags include deposits from scam-linked wallets, exposure to sanctioned addresses, mixer activity, rapid movement across wallets, or repeated transactions below review thresholds.

Challenges Crypto Exchanges Face During Onboarding

Crypto exchanges must balance speed and control. Customers want fast onboarding, but compliance teams need careful checks. If the process is too slow, customers may leave. However, if it is too weak, bad actors may enter.

False positives are another challenge. Screening tools may flag innocent users because their name matches someone on a list. Therefore, analysts need training and clear procedures to resolve matches fairly.

Global document differences, data privacy, and evolving fraud tactics also create pressure. These risks include AI-generated documents, synthetic identities, deepfake selfies, and organized scam networks.

Best Practices for Exchange Compliance Teams

A strong onboarding program should be risk-based. Higher-risk customers should receive deeper review, while lower-risk customers can follow a simpler process.

Exchanges should combine identity, behavior, and wallet data. Identity checks confirm who the customer is. Device and behavior checks show how the account is being used. Wallet screening shows whether funds or addresses carry risk.

Documentation is also important. Analysts should record why a customer was approved, rejected, restricted, or escalated. Support and onboarding teams should receive regular training because they often see early warning signs before the compliance team does.

FAQs About How Crypto Exchanges Verify Customers

How do crypto exchanges verify customers?

Crypto exchanges verify customers by collecting identity details, checking documents, confirming selfies or liveness, screening against risk lists, assessing customer risk, and monitoring account activity.

Why do crypto exchanges ask for ID?

Crypto exchanges ask for ID to confirm identity, reduce fraud, prevent account abuse, support AML controls, and meet legal or compliance expectations.

What is KYC onboarding in crypto?

KYC onboarding is the process of registering, verifying, screening, and risk-rating a customer before they can fully use a crypto exchange.

What is CDD in crypto customer verification?

CDD means reviewing risk beyond basic identity checks, including expected activity, source of funds, account purpose, location, and wallet exposure.

Conclusion

Crypto customer verification is more than collecting an ID. It connects KYC, CDD, sanctions screening, wallet risk checks, manual review, and ongoing monitoring into one practical compliance workflow.

For exchanges, this process helps confirm who customers are, what risk they present, and whether their activity makes sense. However, onboarding is not a one-time task. Customer risk can change, wallet exposure can shift, and new red flags can appear after approval.

Final CTA: Build Practical KYC, CDD, and Onboarding Skills

If you want to understand how crypto exchanges verify customers in real-world onboarding environments, the How Crypto Exchanges Verify Customers: KYC, CDD and Onboarding Explained course is designed for you.

This course helps learners understand how exchange teams review customers, assess risk, identify red flags, handle failed verification, and support safer crypto operations.

Start learning today and build practical crypto onboarding skills for the future of digital asset compliance.